The full-year 2025 financial and volume data of major listed cruise groups not only marks another milestone but shows a widening spectrum of performances among them, revealing clear frontrunners in a highly competitive race.

By Alan Lam

It was not surprising that the latest set of financial figures would unveil another year of record-breaking business performances by the four leading listed cruise groups – Carnival Corporation & plc (CCL), Royal Caribbean Group (RCG), Norwegian Cruise Line Holdings Ltd (NCLH), and Viking Holdings Ltd (VIK). But, in some cases, the results were achieved at a slower pace than in the previous year. This trend was detected in our previous reviews.

What most attracted the attention of analysts and investors was the widening spectrum of performances among the majors. Two frontrunners in this increasingly competitive environment have emerged. VIK and RCG seem to have built on their already stronger results and become more attractive investment options among their peers.

While CCL just reinstated dividend, strengthened its balance sheet, and simplified its capital structure, RCG gladdened shareholders’ hearts by taking a step further and announcing a 50% increase in quarterly dividends, from $1.00 to $1.50 per ordinary share. VIK, at the same time, quietly released a set of even better figures. NCLH, by contrast, moved in the opposite direction: its 2025 performance was found wanting in most areas.

Another milestone

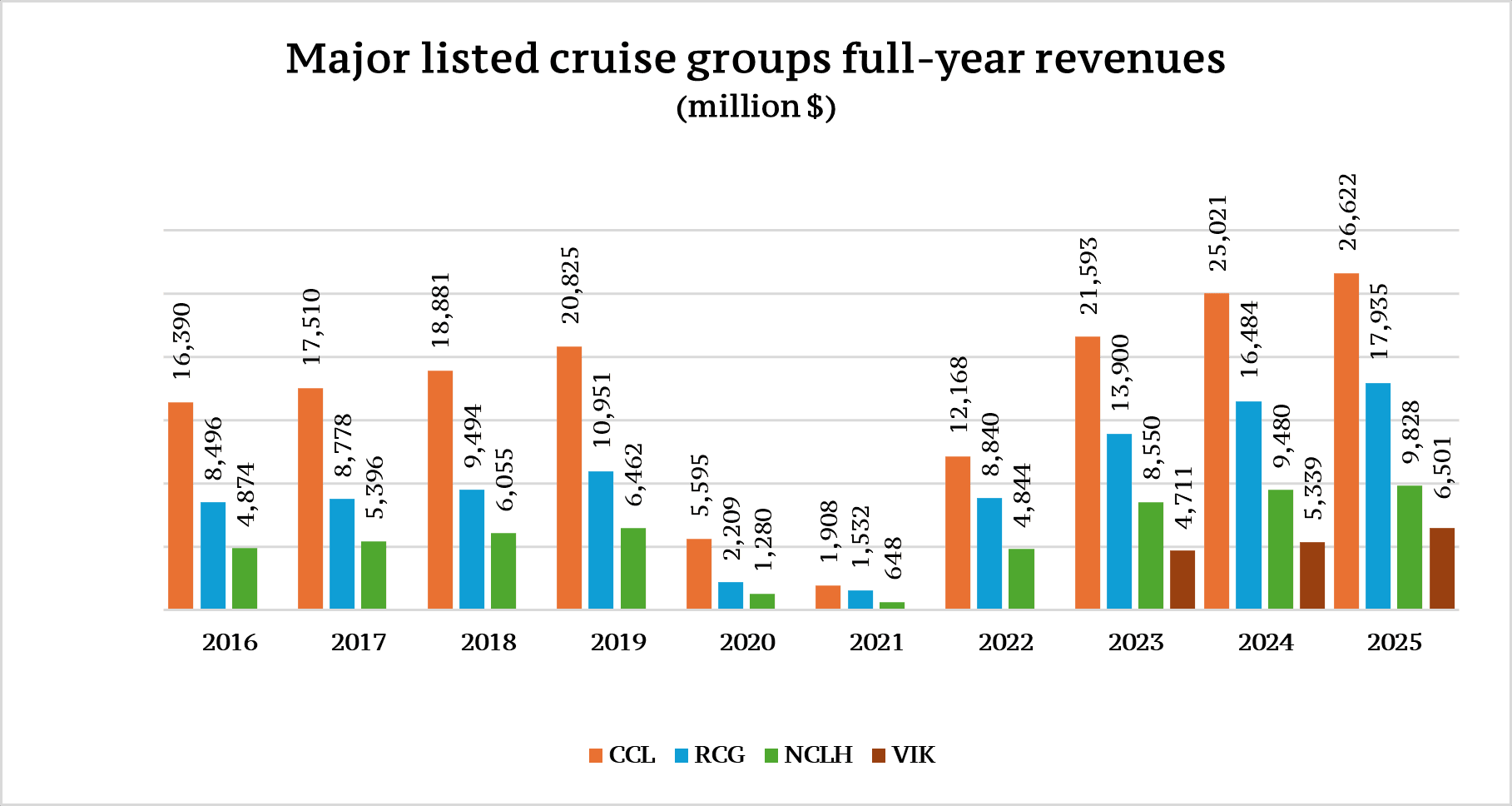

All four listed cruise groups have reported record revenues for the full year 2025. The quartet collectively achieved an 8.1% improvement – another milestone. But this was a conspicuous slowdown, as the corresponding figure for 2024 was almost twice that, at 15.5%.

The pace of increment varied widely. VIK led the field with a 21.8% increase in total revenue, followed by RCG with 8.8%, CCL with 6.4%, and NCLH with just 3.7%.

The recently listed VIK was the only one to have increased the pace of revenue growth in 2025, as its equivalent figure for 2024 was 13.3%. The other three members of the quartet reported a much slower pace in 2025. In 2024, RCG experienced a 57.2% revenue increase, CCL 15.9%, and NCLH 10.9%.

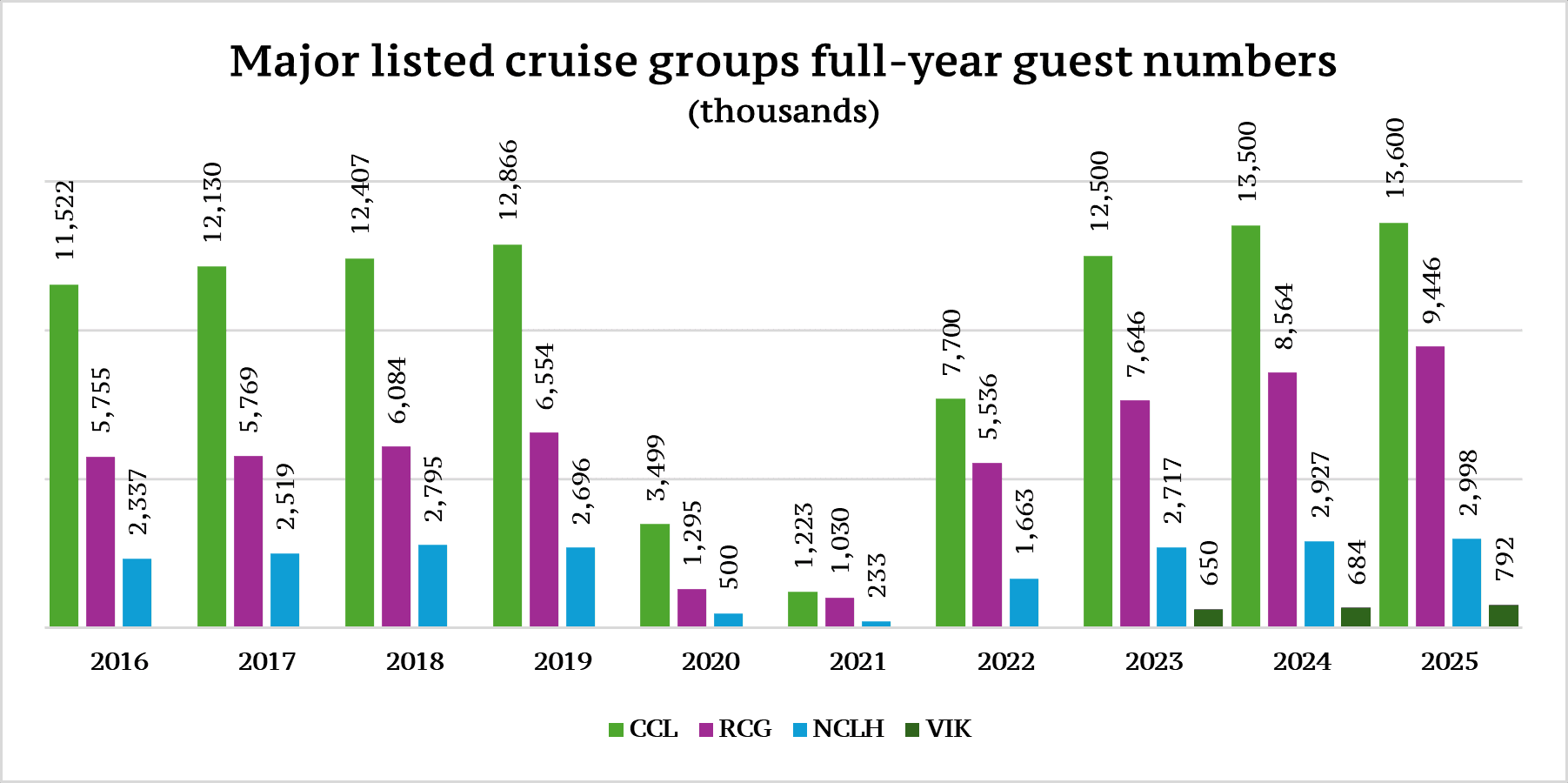

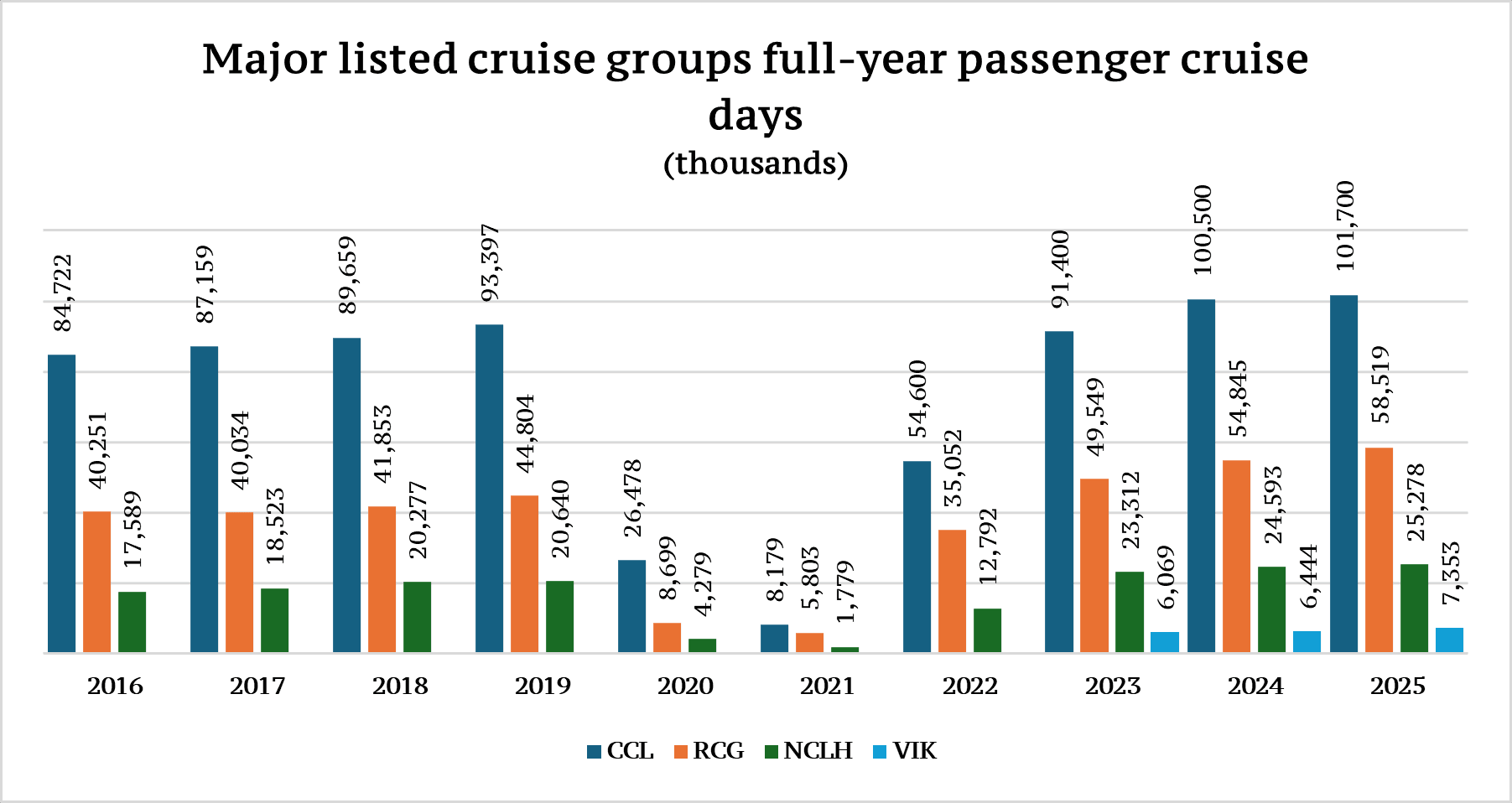

VIK also led the field for guest numbers, with a 15.8% improvement for the full year 2025, followed by RCG at 10.3%. CCL and NCLH experienced only negligible rises of 0.7% and 2.4%, respectively. As for the crucial passenger-day numbers, VIK reported a 14.1% increase, followed by RCG’s moderate 6.7%. The figures for CCL and NCLH were quite insignificant in the current market environment, at 1.2% and 2.8%, respectively.

CCL’s full-year average occupancy rate was 105%, RCG’s was an impressive 109.7%, and NCLH’s was 103.5%. This is one area VIK seems to have underperformed compared to its three bigger contemporaries, with average occupancy for 2025 of just 95.4% (already an improvement on the 93.6% of the previous year). But it must be stressed here that Viking Cruises is an adult-only line, so, in theory, its ships cannot achieve more than 100% occupancy.

For RCG, the virtual maximum occupancy rate, brighter demand outlook, and improved financial performance immediately prompted fresh orders for more newbuilds.

Source: CCL, RCG, NCLH, and VIK

Source: CCL, RCG, NCLH, and VIK

Source: CCL, RCG, NCLH, and VIK

Source: CCL, RCG, NCLH, and VIK

Source: CCL, RCG, NCLH, and VIK

Source: CCL, RCG, NCLH, and VIK

Mirroring patterns

The same patterns found in revenue and volume increases were also evident in earnings performance.

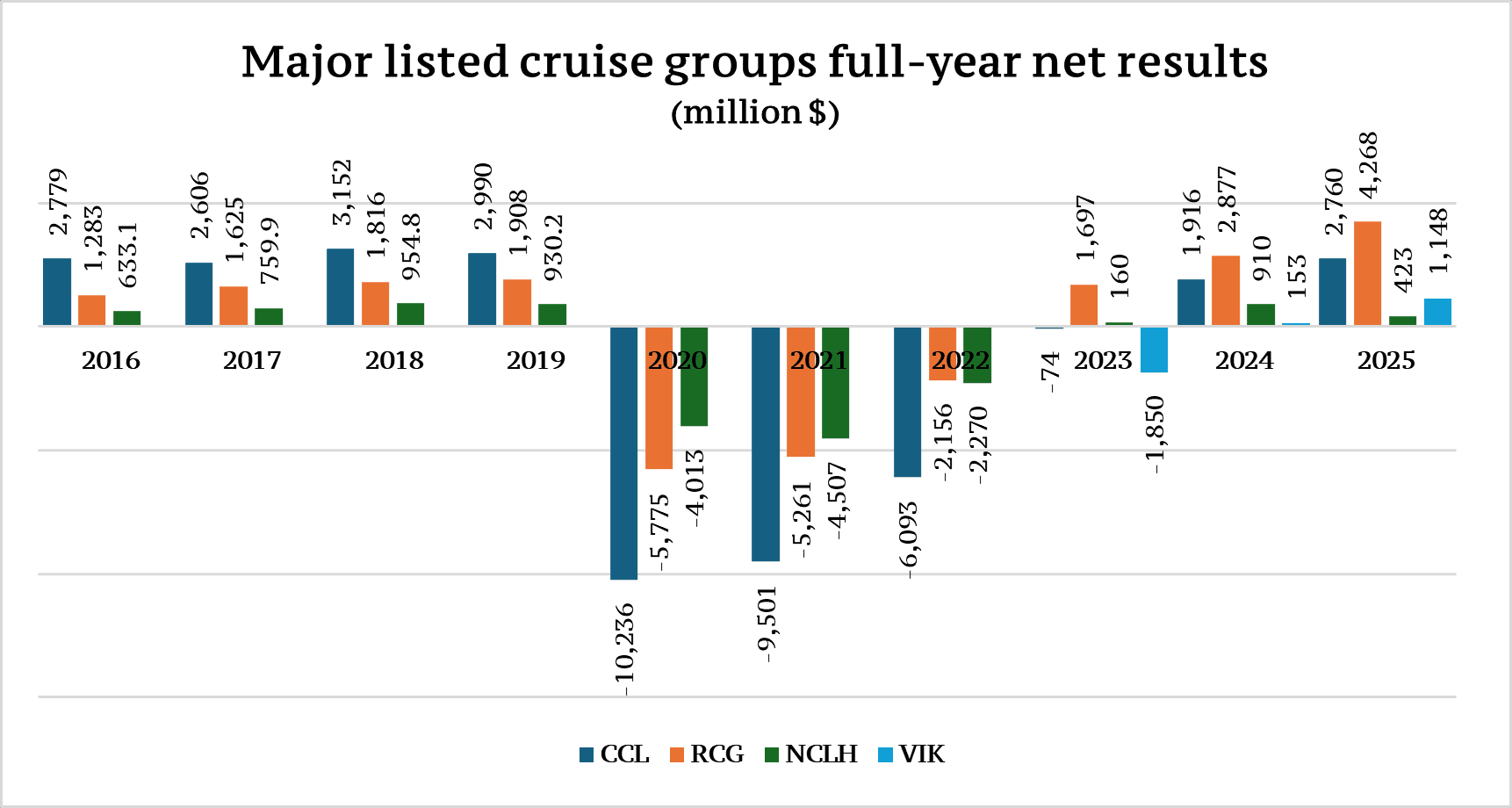

VIK again led the field by a huge margin, with a 650.3% improvement in net result for 2025, followed by RCG with 48.3% and CCL with 44.1%. What is truly unfortunate here is NCLH experiencing a 54% fall in net profit for 2025, compared to its 469% rise in 2024. This was apparently due to “a series of missteps” in its strategy.

These missteps apparently had been taken for years, resulting in the group losing its competitive edge against its peers. As a consequence, even before publication of the full-year results, discontent was brewing among its shareholders. Elliott Investment Management, a hedge fund with more than 10% interest in NCLH, initiated a rebellion, calling for a strategic realignment aimed at reversing the trend. This soon resulted in the departure of the chief executive officer and an extensive restructuring of management.

The new management believes it can turn things around. According to John W. Chidsey, NCLH’s incumbent president and CEO, “our strategy is sound, but execution and cross-functional alignment have fallen short. Our priority is to act urgently to address these gaps by improving coordination, reinforcing accountability, and strengthening financial discipline across the organisation.”

The new management believes it can turn things around. According to John W. Chidsey, NCLH’s incumbent president and CEO, “our strategy is sound, but execution and cross-functional alignment have fallen short. Our priority is to act urgently to address these gaps by improving coordination, reinforcing accountability, and strengthening financial discipline across the organisation.”

NCLH – unlike CCL and RCG – has not reinstated dividend for 2025. But it must be stressed that it is still a profitable company. It recorded an operating income of $1.56 billion for 2025, a 6.5% improvement on the previous year, and its EBITDA for the same 12-month period was $2.73, an 11.4% increase on 2024. So the picture may not be as disheartening as it has been painted.

But there is little doubt about the more robust earnings performances of VIK, CCL, and RCG. This, though offering little comfort to NCLH’s shareholders, points to the general brighter prospect for all.

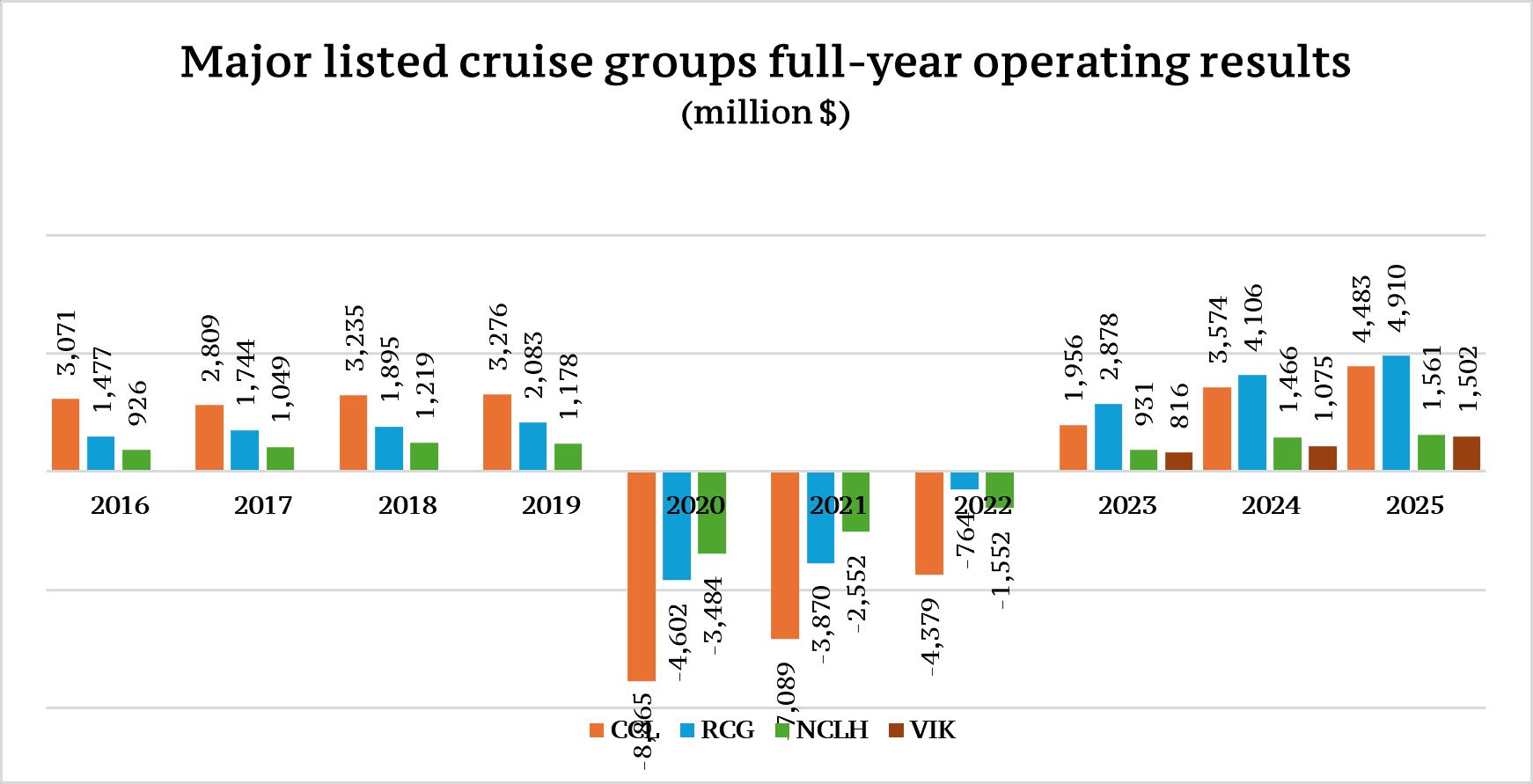

CCL’s revenue increase continued to outpace that of its operating expenses, which rose by just 2% in 2025, resulting in a 25.4% improvement in operating income – though the figure for the previous year was an incredible 82.7%. The company also reported a 17.6% increase in adjusted EBITDA, but again, the corresponding figure for 2024 was 44.4%.

RCG’s operating income increased by 19.6%, a drop from the inspiring 42.7% of 2024. There was also a slowdown in net income improvement in 2025, which fell from 69.5% in 2024 to 48.4% in 2025 – still a noteworthy figure. Its pace of improvement in adjusted EBITDA also slowed, from 31.4% in 2024 to just 17.7% in 2025.

Having outpaced Wall Street expectations, VIK was the champion earnings performer among its peers. The company reported a 39.7% improvement in operating income, compared to 31.7% in 2024, and a 38.9% increase in EBITDA, compared to 23.7% in 2024.

VIK is powering ahead. Its pace has increased, unlike that of its three bigger peers. Confident about its prospect, on the occasion of publishing its fourth-quarter and full-year 2025 financial review, the company announced having ordered two more expedition newbuilds and added options.

Source: CCL, RCG, NCLH, and VIK

Source: CCL, RCG, NCLH, and VIK

Source: CCL, RCG, NCLH, and VIK

Source: CCL, RCG, NCLH, and VIK

Source: CCL, RCG, NCLH, and VIK

*CCL figures include tour costs

EPS indicator

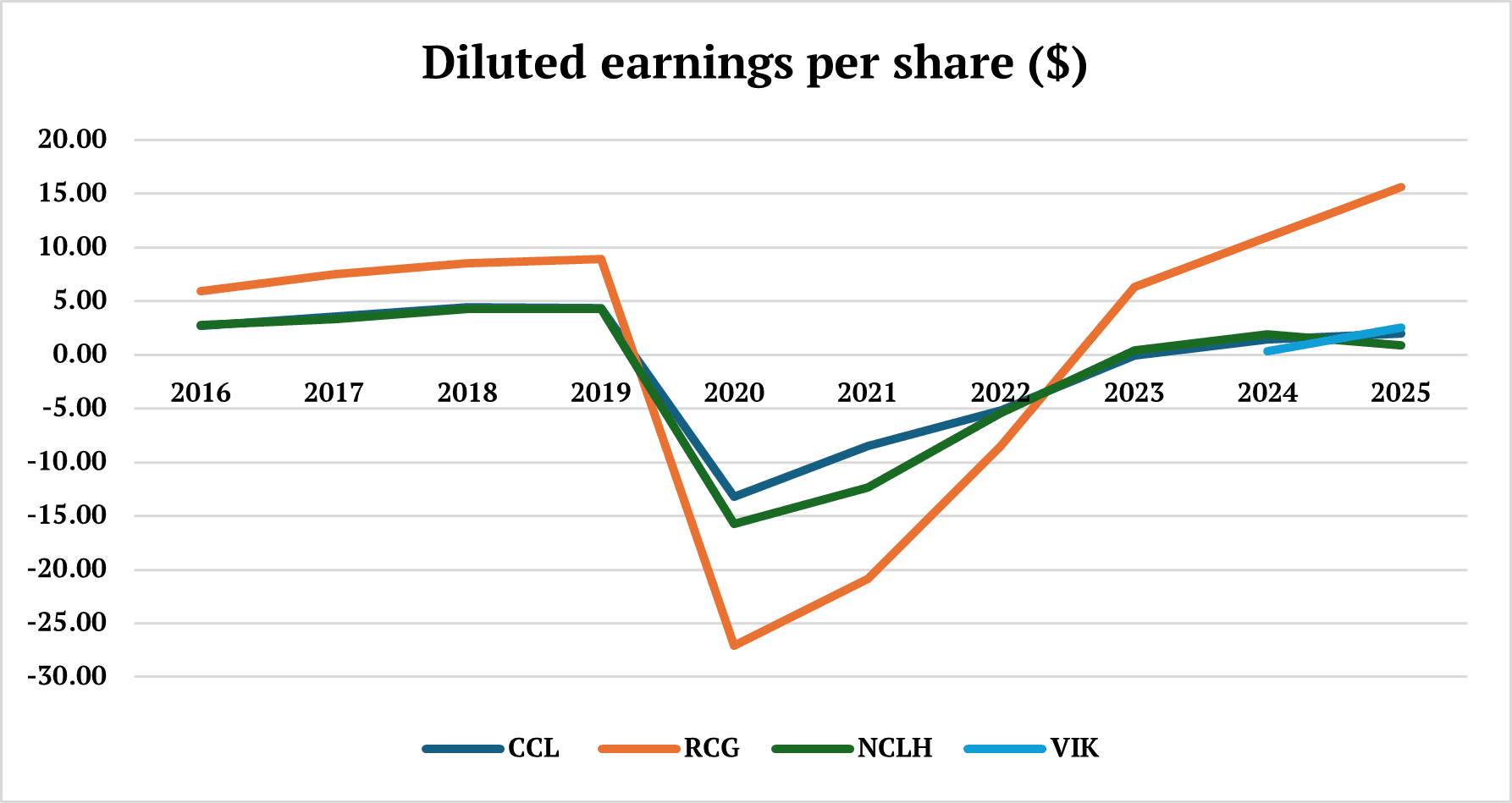

One of the best indications of financial health is perhaps the earnings per share (EPS) figure. In this regard, VIK again was the frontrunner. It reported a 613.9% improvement in diluted EPS in 2025 over the previous year, rising from $0.36 to $2.57. By any measure, this is quite an achievement in such a short time.

RCG recorded a 42.7% improvement in EPS, from $10.94 in 2024 to $15.61 in 2025. This figure was 74.4% higher than in the pre-pandemic peak year of 2019.

Neither of the remaining two majors was able to match the success of VIK or RCG. CCL’s diluted EPS rose from $1.44 in 2024 to $2.02 in 2025. Although this represented a respectable 40.3% improvement, it fell short of its 2019 record by 53.2%.

In this regard, NCLH’s failing is most salient. Its EPS fell by 51.3%, from $1.89 in 2024 to just $0.92 in 2025 and a long way from the $4.30 of the pre-pandemic peak – a thoroughly depressing picture for its investors.

It is interesting to note that this divergence in performance has occurred since the pandemic. In the years leading up to 2020, the majors’ EPS performances were quite even.

Source: CCL, RCG, NCLH, and VIK

Bright prospect

All the indicators so far suggest that the prospect for the sector remains bright for all, in spite of the slowing of pace for some.

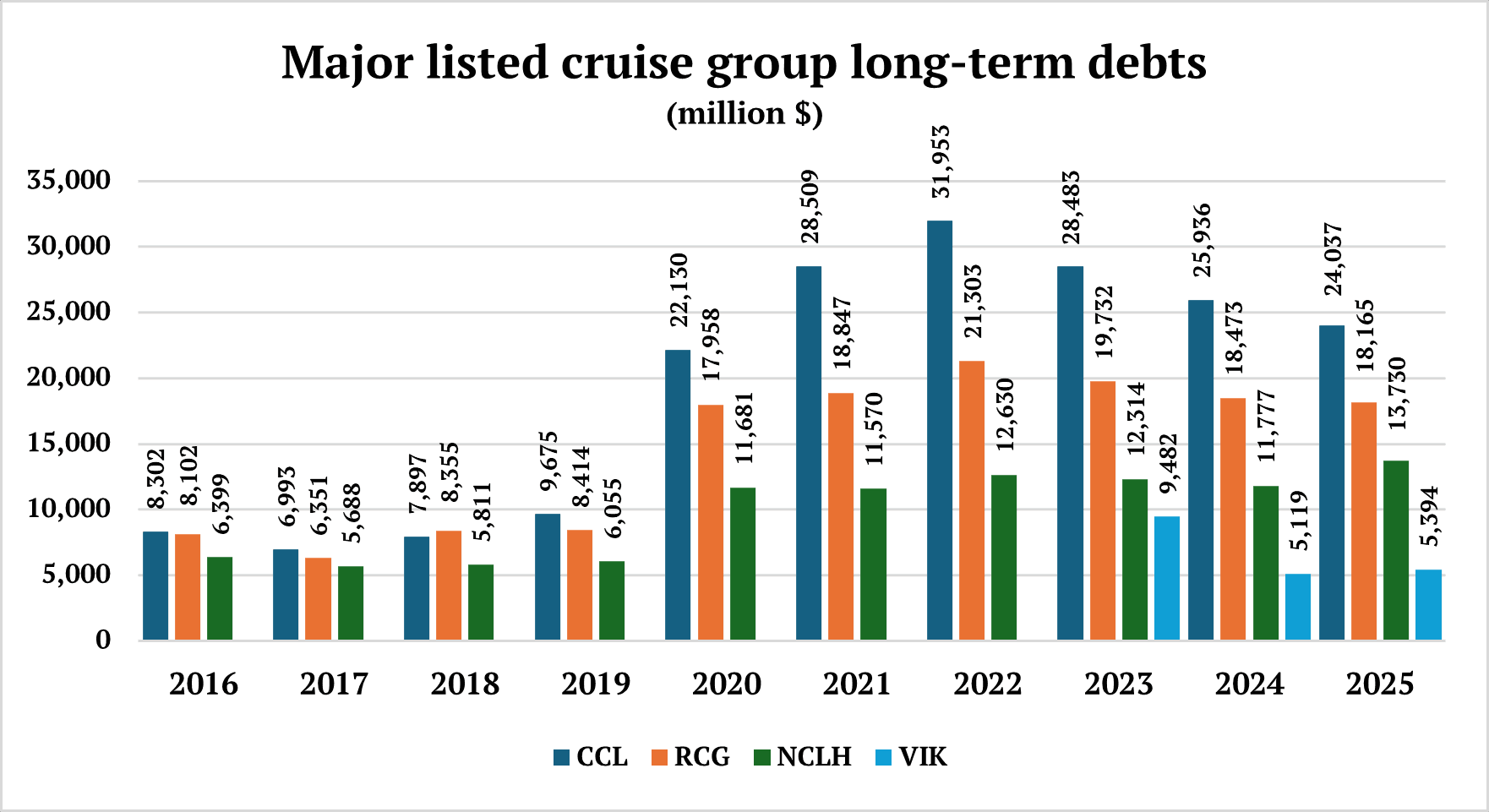

Through continuous restructuring and refinancing, debt levels – except for NCLH’s, which rose 17% in 2025 because of its missteps – are now broadly under control, though not falling as fast as was hoped for. VIK also experienced a rise in long-term debts at the end of 2025, by about 5.4%. We could see it rising further because of the new ships the company is building for both its ocean and river segments.

Source: CCL, RCG, NCLH, and VIK

Source: CCL, RCG, NCLH, and VIK

The general sentiment of the sector is, as always, one of confidence. “Looking forward, we are well positioned to top 2025’s record yields,” said Josh Weinstein, CCL’s chief executive officer. “We remain at our highest booked occupancy for the upcoming year at about two-thirds booked at higher prices (in constant currency). In fact, we’re at historical high prices (in constant currency) for both North America and Europe.”

The general sentiment of the sector is, as always, one of confidence. “Looking forward, we are well positioned to top 2025’s record yields,” said Josh Weinstein, CCL’s chief executive officer. “We remain at our highest booked occupancy for the upcoming year at about two-thirds booked at higher prices (in constant currency). In fact, we’re at historical high prices (in constant currency) for both North America and Europe.”

Under normal circumstances, we see no reason why the sector would not continue to improve on its performance in the coming years. But the circumstances may not remain normal for long.

Positive stance

Despite the slowing trend, management is taking a positive stance and is defiant about the business performance and outlook. “2025 was a truly phenomenal year,” said Weinstein. “We set new records across our business, achieved investment grade leverage metrics and reinstated our dividend. These milestones reflect the collective strength of our cruise line portfolio and confidence in our long-term future.”

RCG’s management had more reason to be confident. “2025 was an outstanding year, and the momentum is further accelerating into 2026. We expect another strong year of financial performance with both revenue and earnings growing in double digits, and we remain on track to achieve our Perfecta goals by 2027,” said Jason Liberty, RCG’s chairman and CEO.

RCG’s management had more reason to be confident. “2025 was an outstanding year, and the momentum is further accelerating into 2026. We expect another strong year of financial performance with both revenue and earnings growing in double digits, and we remain on track to achieve our Perfecta goals by 2027,” said Jason Liberty, RCG’s chairman and CEO.

VIK’s management certainly did not have to be apologetic about their celebratory mood. “We finished 2025 with great momentum, and we are entering 2026 in a very solid position with 86% of our Capacity PCDs for our core products already sold,” said Leah Talactac, VIK’s president and chief finance officer. “We are seeing a strong

booking environment characterised by robust demand across our products, from both repeat guests and new-to-brand customers.”

For the moment, at least, VIK is a clear frontrunner among its peers. It is stretching the performance spectrum forward and upward.