The three major cruise groups have broadly delivered another set of strong results despite the increasing economic uncertainty and polarisation in the world. But there are concerns and signs of softening.

By Alan Lam

The US tariff regime and intense geopolitical activity initially caused a measure of concern and market disturbance in the cruise sector. But these anomalies were then broadly shrugged off as mere bumps on the road.

The cruise industry’s enviable ascent still seems unstoppable, going by most of the latest performance figures of the three major listed cruise conglomerates. The overused phrase “better than expected” typifies their interim financial performance – resulting, in most cases, in yet another raise in full-year guidance.

The sector remains steadfast and unperturbed by the evolving new world order and constant policy changes. But there are also concerns, as one of the three majors reported a weaker six-month performance.

Notable concerns

In its Q1 review, Norwegian Cruise Line Holdings Ltd (NCLH) reported a softening of demand, with a 3% drop in revenue, a net loss of more than $40 million (down from a net income of $17.4 million in the same period in 2024), and a negative EPS of −$0.09. Its passenger volume fell by 9%, and passenger cruise days fell by 9.5% – fairly steep drops.

This unexpected reversal of fortune raised a number of concerns. Because the Q1 period coincided with the inauguration of the new administration in the USA, which threatened to tax cruise ships and implemented unreasonable trade tariffs worldwide, could this be the cause of the sudden softening of demand?

While it may have influenced the outcome in some ways, we see a more fundamental issue here, one of macroeconomic performance. What was more concerning was that, besides the actual numbers falling in Q1, NCLH acknowledged that forward bookings have softened too. “The company has seen softening in its 12-month forward booked position but continues to remain within the optimal range, even amid ongoing macroeconomic volatility,” the company stated.

What must be particularly frustrating for NCLH is that its nearest rival, Royal Caribbean Group, did not suffer this setback. On the contrary: RCG reported a 7% rise in revenue for Q1, and net income more than doubled. It recorded a 9% increase in passenger volume and a 5% rise in passenger cruise days. It also increased its full-year guidance. This performance result counters the hypothesis that the new US government policies negatively impacted the cruise industry.

But could NCLH’s Q1 business performance be the first warning sign of a weakening market after a strong run? The company clearly feels the continuing cost pressure and intends to place major emphasis on addressing it. “While we recognise there may be potential pressures on the top line, we believe these can be effectively offset by the continued execution of our cost savings initiatives,” said Harry Sommer, the group’s president and CEO. “Our focus remains on managing the business for the long term – balancing disciplined pricing and cost control with guest experience and strategic investments for the future.”

NCLH was confident about its strategy and maintained its previous guidance. The subsequent Q2 result, despite a record revenue of $2.5 billion, among other bright spots, failed to lift the sombre spirits. But the company remained upbeat about the full-year performance: “Demand has rebounded across all three of our brands, with bookings now ahead of historical levels in recent months and continued strength in onboard spend,” said Sommer.

Bigger picture

Overall, in the first six months of 2025, NCLH’s experience was not shared by its two larger peers. Neither Carnival Corporation & plc (CCL) nor RCG suffered this level of setback.

“We have already exceeded our 2026 SEA Change financial targets a full 18 months early, increasing adjusted EBITDA per ALBD by 52% and more than doubling adjusted ROIC to over 12.5% in less than two years,” said Josh Weinstein, CEO of CCL. “Our strong results, booked position, and outlook are a testament to the success of our ongoing strategy to deliver same-ship, high-margin revenue growth. We continue to set ourselves up well for 2026 and beyond, with so much more potential to take our margins, returns and results even higher over time.”

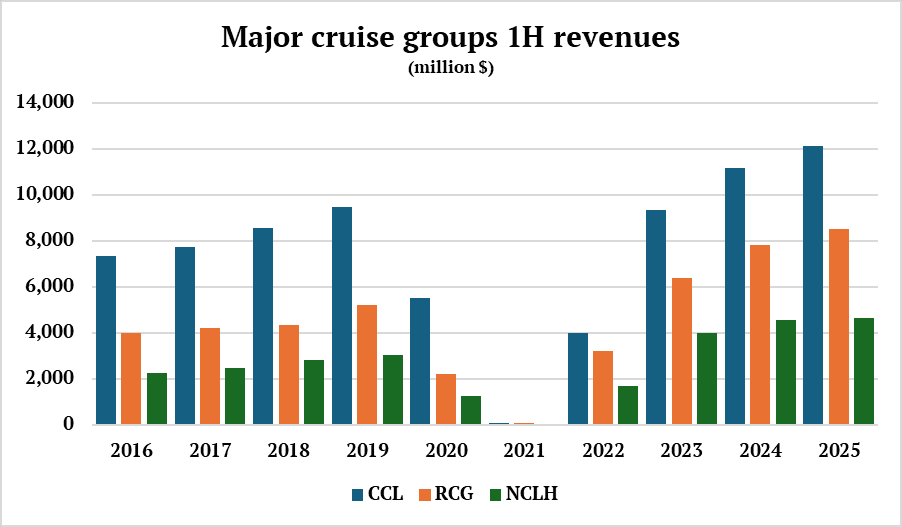

CCL reported an 8.5% rise in revenue for the first six months of 2025, compared to its 2024 figure. RCG reported a 9% increase in revenue compared to 2024. NCLH registered only a 1.8% revenue increase in the same period, brought about mainly by a relatively stronger Q2 performance, which compensated for the drop in Q1.

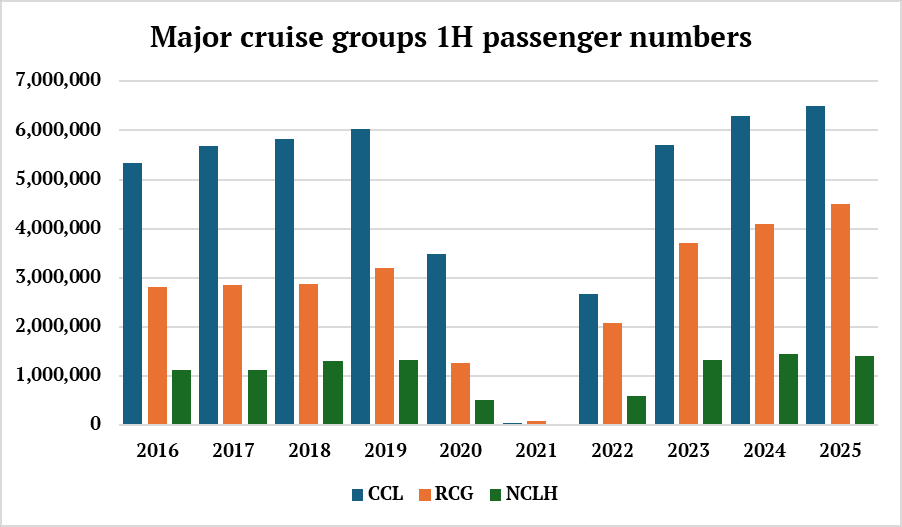

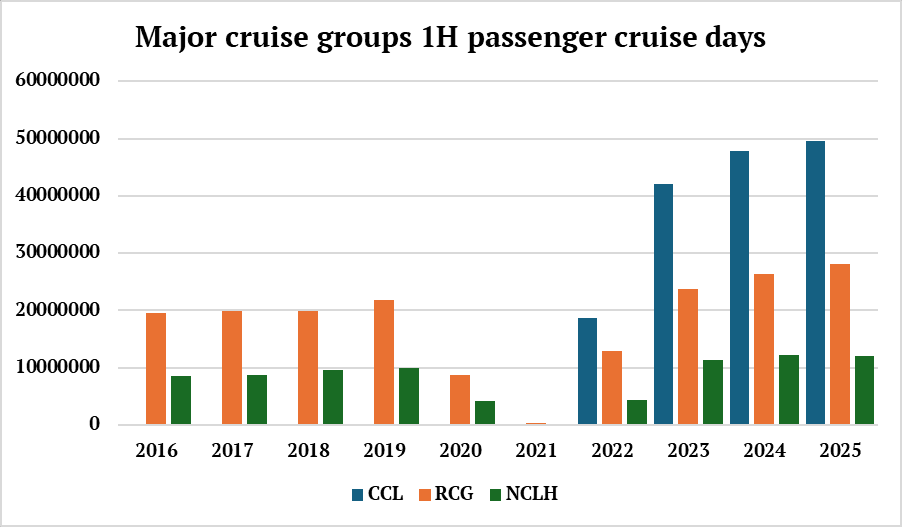

In line with the revenue trend, CCL’s passenger volume rose by 3.2%, and its passenger cruise days increased by a corresponding 3.8%, compared to 2024. RCG’s respective percentage figures were much higher, at 10% and 6.3%. Unfortunately, NCLH’s six-month passenger volume suffered a 2.8% drop, and its passenger cruise days fell by nearly 1%. In a strong market, this was a sorely inadequate performance.

Again, the question is whether this could be a portent of softening for the entire sector. Could NCLH be leading a flatlining or even downward trend? So far, the performances of the other two giants have by and large indicated otherwise.

Given its recent track record, RCG unsurprisingly emerged as the strongest performer among its peers. “Demand for our portfolio of brands and our industry-leading experiences continues to accelerate,” said Jason Liberty, RCG’s president and CEO. “Grounded in our mission to deliver the best vacations responsibly, we remain keenly focused on delivering exceptional value for our guests and shareholders – not just by executing today, but by staying ahead of where demand is going.”

The prospect for RCG thus remains rosy. The company’s business performance seems to be going from strength to strength. “We are well on our way to achieving our Perfecta financial targets by the end of 2027,” Liberty said. “As we look beyond 2027, we see another step change in growth as we deepen our moat with a powerful pipeline of incredible new ships, the ramp-up of our highly differentiated new destinations and river cruising, and continued investments in disruptive technology, personalisation and loyalty.”

Source: CCL, RCG, NCLH

Source: CCL, RCG, NCLH

Source: CCL, RCG, NCLH

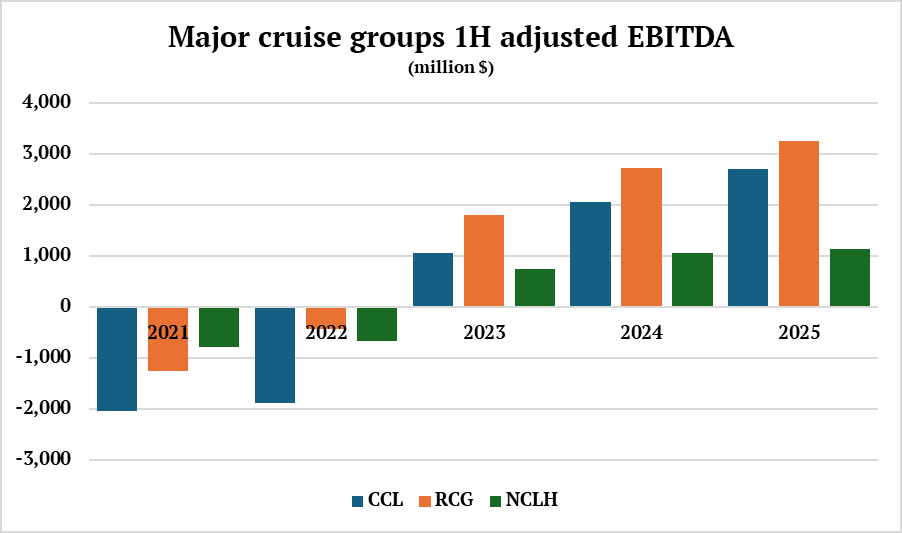

Wider margin

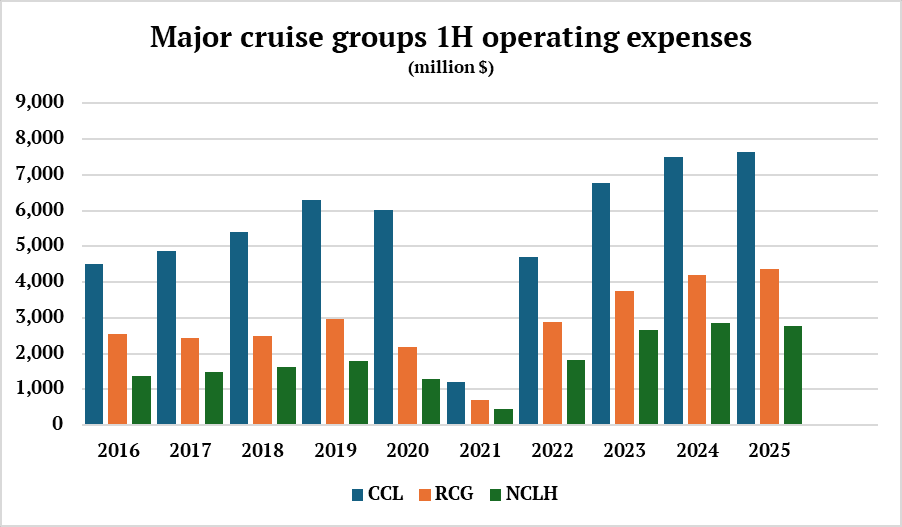

What is noticeable is that the operating expenses of both CCL and RCG rose only slightly, by 2% and 3.7%, suggesting a wider profit margin. In NCLH’s case, the figure actually fell by nearly 3%.

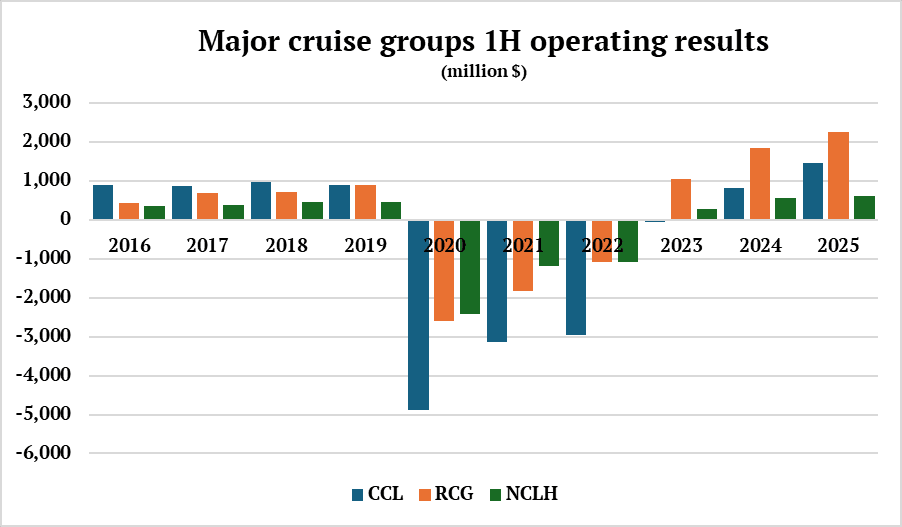

This indicates excellent cost management, which is reflected in the EBITDA. This rose by a massive 31.2% for CCL and by 19.3% for RCG; even NCLH reported a 9% increase for the period. The operating results are still more impressive, with CCL reporting a 76.7% leap, RCG 23.1%, and NCLH 11.6%, compared to their 2024 figures.

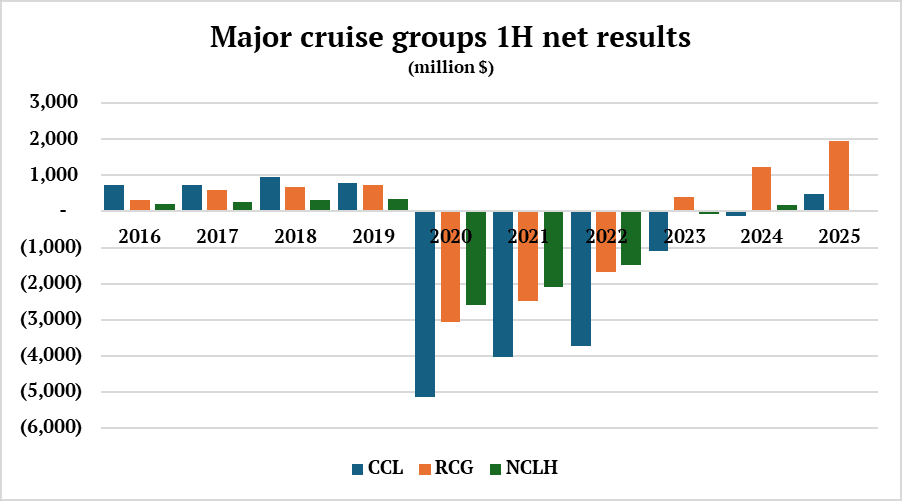

In terms of six-month net results, RCG was again the star performer, with a figure of $1.95 billion, a 60% improvement on the already extraordinary performance of the same period in 2024, outperforming its nearest rival by a huge margin. CCL’s six-month net result turned positive for the first time since 2019, while NCLH headed in the opposite direction: it reported a $10.3 million net loss in the first half of 2025, after its net result turned positive in the first half of 2024. In this regard, figures for CCL and NCLH are a somewhat concerning sign for the sector.

Source: CCL, RCG, NCLH

Source: CCL, RCG, NCLH

Source: CCL, RCG, NCLH

Source: CCL, RCG, NCLH

Good sentiment

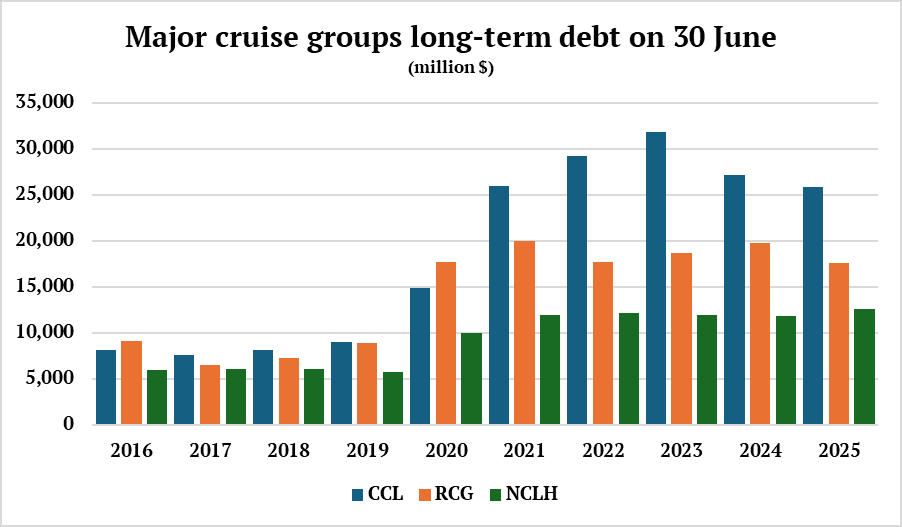

Major cruise groups are still operating in a high-debt environment, the levels of long-term debt are still much higher than in the years before Covid-19. The long-term debt of NCLH, against the general trend, has actually risen by 6% between June 2024 and June 2025. This could be a symptom of its weaker financial performance so far this year.

Operating under such an oppressive debt regime makes these cruise groups vulnerable to interest rates rising or credit markets tightening. And with their expanding newbuilding programmes, long-term debts may be a heavy pressure for years to come.

While the cruise market overall remains robust, with demand continuing to rise, there have been tangible signs of weakening in the first six months of 2025, as demonstrated by NCLH’s interim results.

This may be just temporary, since all other signs remain upbeat. Equally, there may be other forces, as yet unidentified, at work here. What is also certain is the overall good sentiment; NCLH’s share price rose by more than 8% on the day these latest results were published, indicating that the market shares the company’s confidence in its full-year performance.

Source: CCL, RCG, NCLH