The latest nine-month financial performance figures of the three major listed cruise groups are clear evidence of a slowdown, confirming earlier indications.

By Alan Lam

Earlier in 2025, based on the Q1 results of the three major listed cruise groups, CruiseTimes detected signs of softening growth in the industry and highlighted the issue in the last performance review. These early signs were confirmed by the recent nine-month figures. While demand remains robust, the pace of growth has definitely slowed.

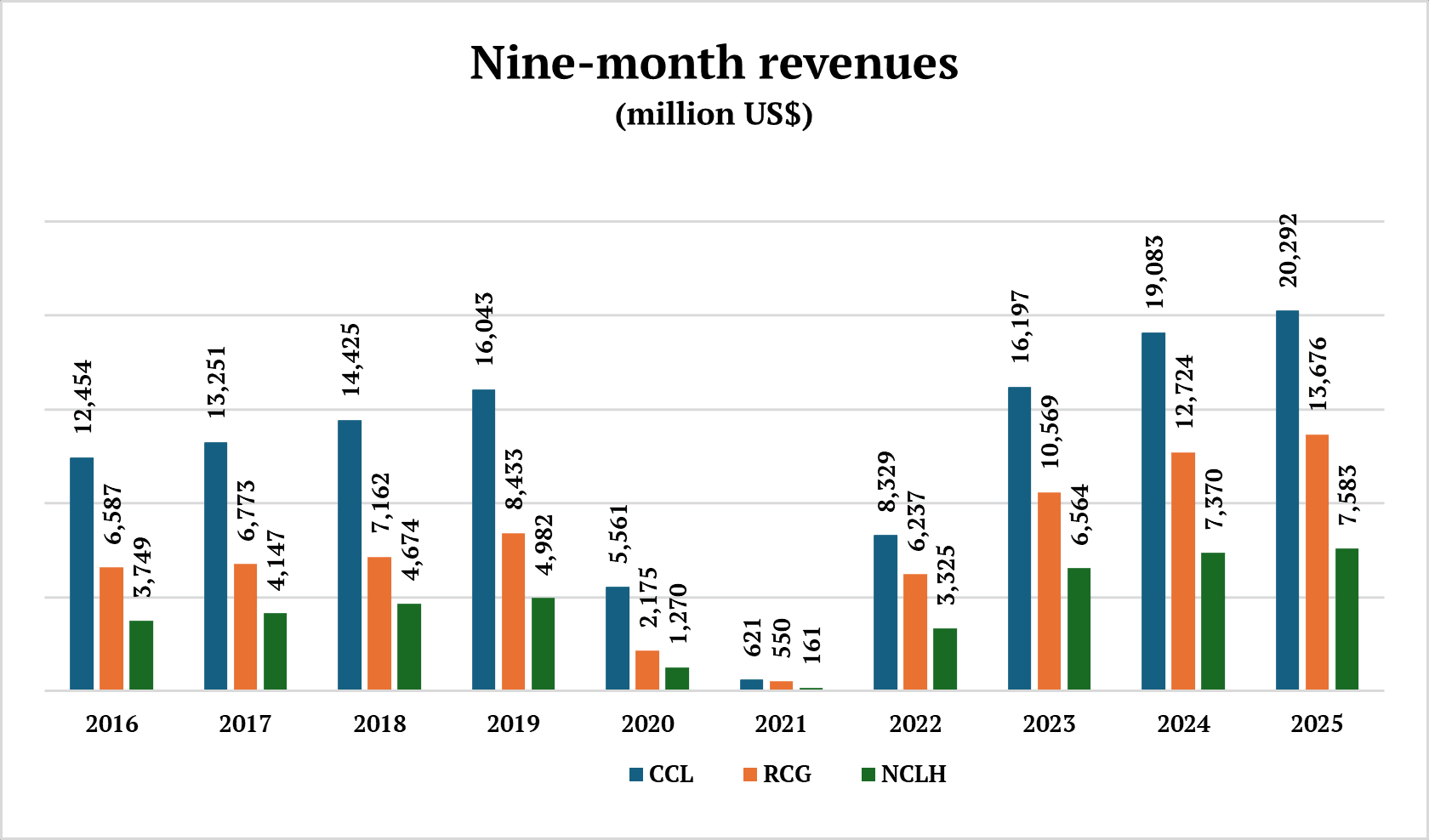

Revenue performances of the three leading cruise conglomerates – Carnival Corporation & plc (CCL), Royal Caribbean Group (RCG), and Norwegian Cruise Line Holdings Ltd (NCLH) – showed an unmistakable trend of slower growth in the first nine months of 2025, alongside smaller increases in passenger numbers and cruise days.

Though these might be cause for concern, the industry as a whole is still flying high, with record-breaking financial results. Its cost-efficiency drives have produced remarkable results, with operating expenses increasing only slightly on bigger volumes of passenger throughput, resulting in wide and comfortable income margins.

Above all, forward demand continues to be strong. The entire sector is still in the “sweet spot” described a year ago by Giles Hawke, Celebrity Cruises’ vice president and managing director for the UK, Ireland, and EMEA.

Slowing down

But the panoramic picture may be a little less rosy. Although the major trio, by and large, are still setting new revenue and earnings records, their latest business performance figures reveal a palpable slowdown.

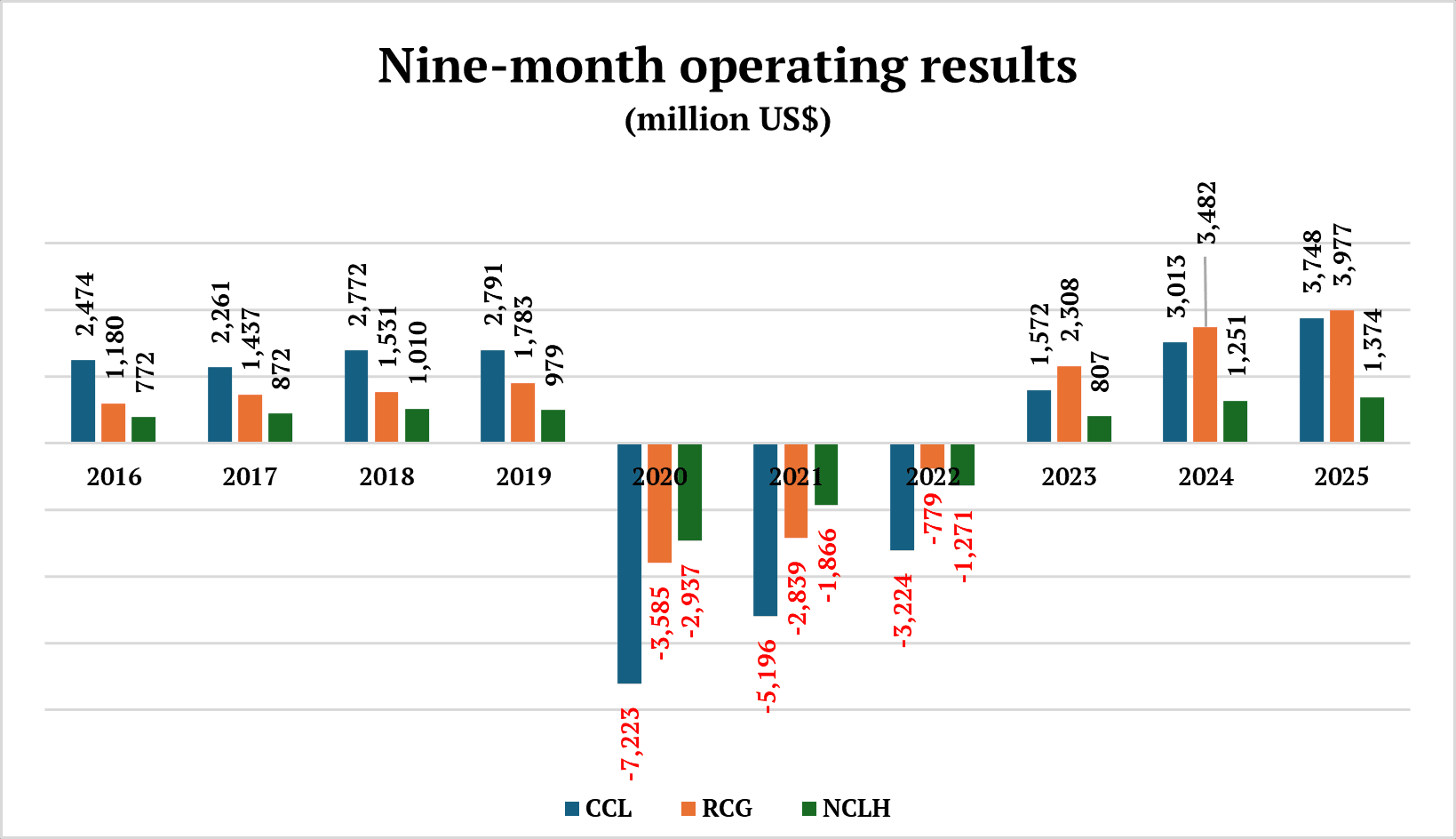

Over the nine-month period, CCL managed to increase its total revenue by a relatively modest 6.3%, compared with 17.8% in the same period in 2024 – a substantial slowdown.

Though RCG is a higher flyer among its peers, the slowdown in its revenue increase is just as noticeable. For the first nine months of 2025, it reported a 7.5% increase in total revenue, compared with 20.4% in the same period in 2024.

NCLH, meanwhile, despite a record quarterly revenue of $2.94 billion for Q3 2025 – up 5% on the comparable figure in 2024 – registered an increase of only 2.9% for the first nine months of 2025, falling from 12.3% in the previous year: a marked slowdown.

Source: CCL, RCG, NCLH

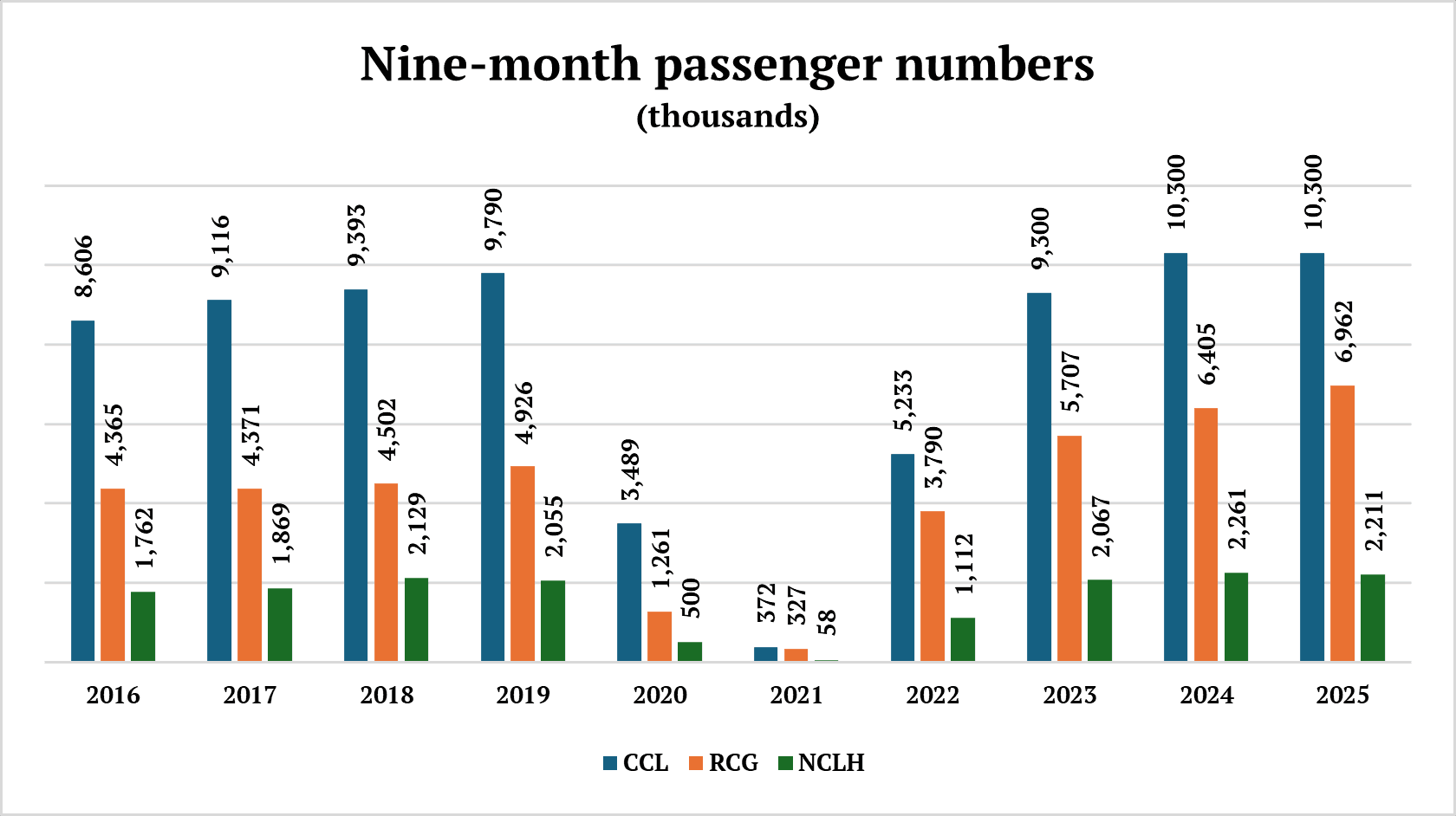

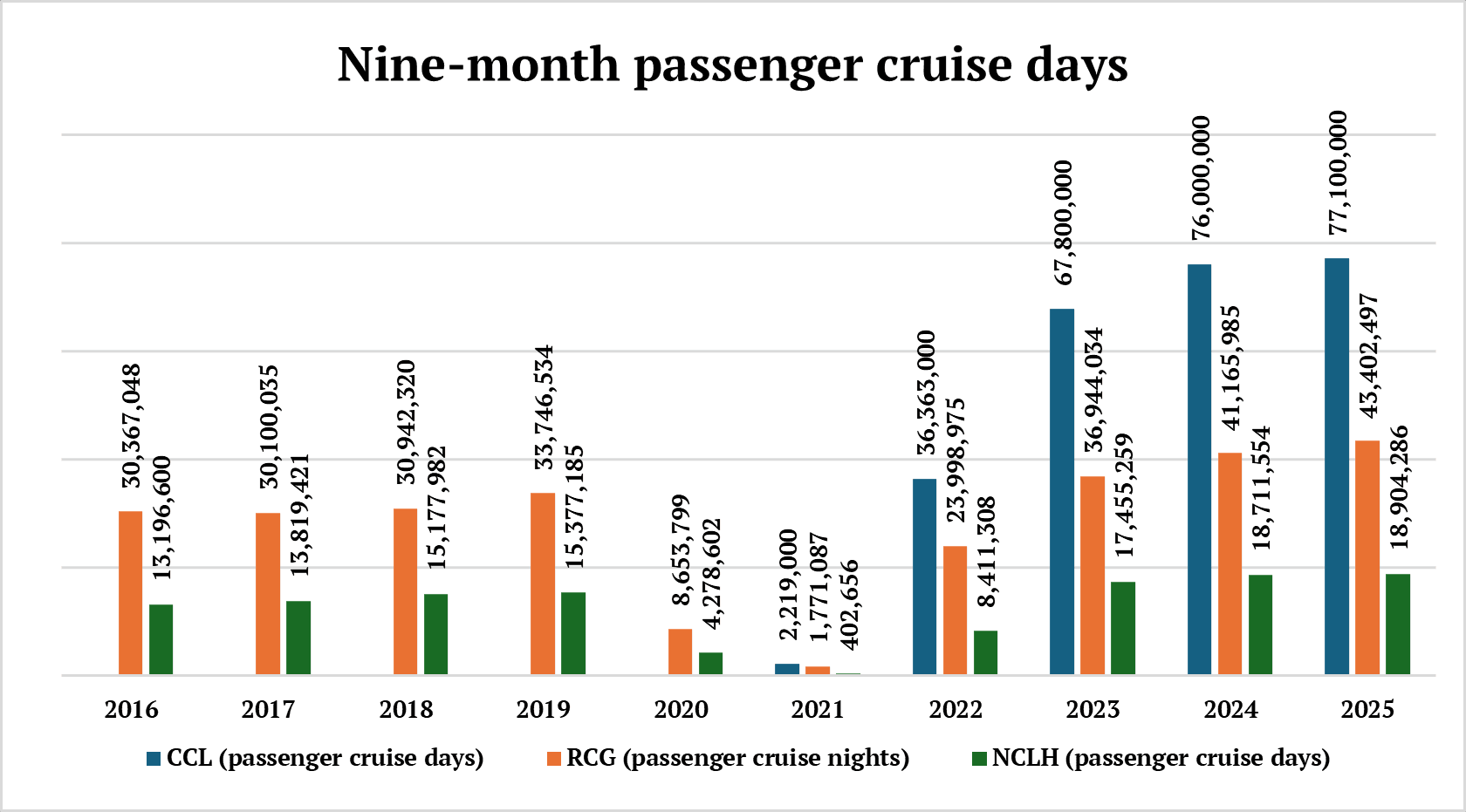

As on all previous occasions, the slowdown in the trio’s revenue performance improvements was a direct result of slower increases in passenger number and passenger cruise days.

CCL’s nine-month passenger number remained unchanged, compared to an 11% increase in 2024. Its passenger cruise days rose by just 1.5%, compared to 12% in the same period in 2024. The increase in revenue being far greater than that of passenger number and cruise days suggests both a higher yield and a flatlining of volume performance.

While there is reason to be cautious, there is also cause for optimism. CCL’s Q3 performance was extraordinary by any measure. The underlying demand was strong for the quarter, with 112% occupancy, and the figure for the nine-month period was 107%. “Since May, booking trends have continued to strengthen with higher booking volumes than last year and far outpacing capacity growth,” said Josh Weinstein, CCL’s CEO.

RCG reported a better 8.7% increase in passenger number for the first nine months of 2025, compared to 12.2% for the same period in 2024. It recorded a 5.4% increase in passenger cruise nights, falling from 11.4% the previous year. While this pointed to a considerable slowdown, again the underlying demand strength was still apparent. For Q3, its load factor was also 112%, while for the nine-month period the figure stood at 110.4%.

For NCLH, by contrast, there was little evidence of increasing strength in these regards. The group actually reported a 2.2% fall in its nine-month passenger number, compared to a 9.4% increase in the same period in 2024. Passenger cruise days improved by only 1%, compared to 7.2% in 2024. Its nine-month occupancy fell from 106.2% to 104%.

Source: CCL, RCG, NCLH

Source: CCL, RCG, NCLH

Source: CCL, RCG, NCLH

Satisfying earnings

In spite of their slower revenue growth, the trio’s overall earnings were nevertheless satisfying, with record Q3 figures.

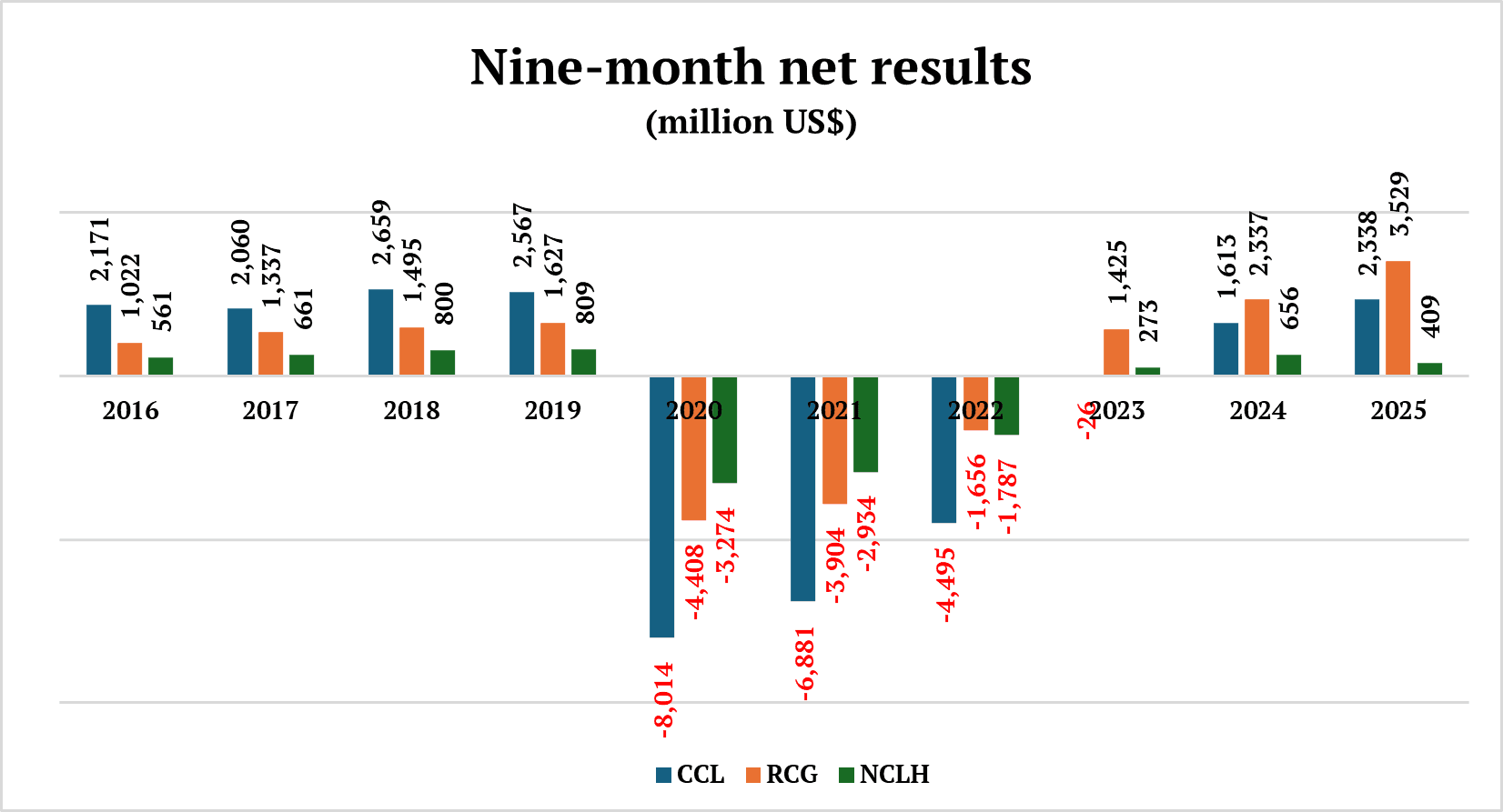

CCL achieved record net income of $1.85 billion for Q3, a moderate 6.7% increase on 2024. Over the nine-month period, the increase was 45%, a much more impressive margin. The company also achieved a record adjusted EBITDA of just under $3 billion for Q3, representing a modest 6.1% increase; while the figures for the nine-month period stood at above $5.7 billion and 16.7%.

“This was a phenomenal quarter, delivering all-time high net income and our tenth consecutive quarter of record revenues,” said Weinstein. “Strong demand and onboard spending drove a 4.6% improvement in net yields (in constant currency), all of which was achieved on a same ship basis.”

But CCL’s Q3 operating income registered only a 4.3% increase on the figure for the same period in 2024, while the nine-month figure was 24.4%.

RCG reported a more respectable 41.6% increase in net income for Q3 and 51% for the nine-month period. But its Q3 adjusted EBITDA increase was a modest 6.8%, and the figure for the nine-month period was 13.8%. RCG’s operating income for Q3 registered only a 4.2% increase on the figure for the same period in 2024, while the nine-month figure was 14.2%, compared to an impressive 50.9% in 2024.

NCLH reported a 9.8% increase in nine-month operating income, compared to 55.1% in the same period in 2024. At the same time, disappointingly, its net income fell by 37.7%; in the same nine-month period in 2024, it achieved a 140.6% improvement over 2023. The group reported a 9.2% increase in EBITDA during the period, falling from the 32.1% increase recorded in 2024.

Source: CCL, RCG, NCLH

Source: CCL, RCG, NCLH

Source: CCL, RCG, NCLH

Source: CCL, RCG, NCLH

It would appear that the earnings growths, while satisfying, have weakened as the year has progressed. But the upbeat sentiment has not been dampened. “We continue to see strong momentum across our business, powered by accelerated demand, growing loyalty, and guest satisfaction that is at all-time highs. Looking ahead, while it’s still early in the planning process, our strong booked position gives us confidence for 2026 and beyond,” said Jason Liberty, RCG’s president and CEO.

RCG was not alone in its optimism. NCLH, despite its relatively weaker position, also saw an encouraging future performance in the making. “The company continues to experience healthy consumer demand across its portfolio of three brands for the balance of 2025 and into 2026, with record bookings made in the third quarter,” it stated.

Overall picture

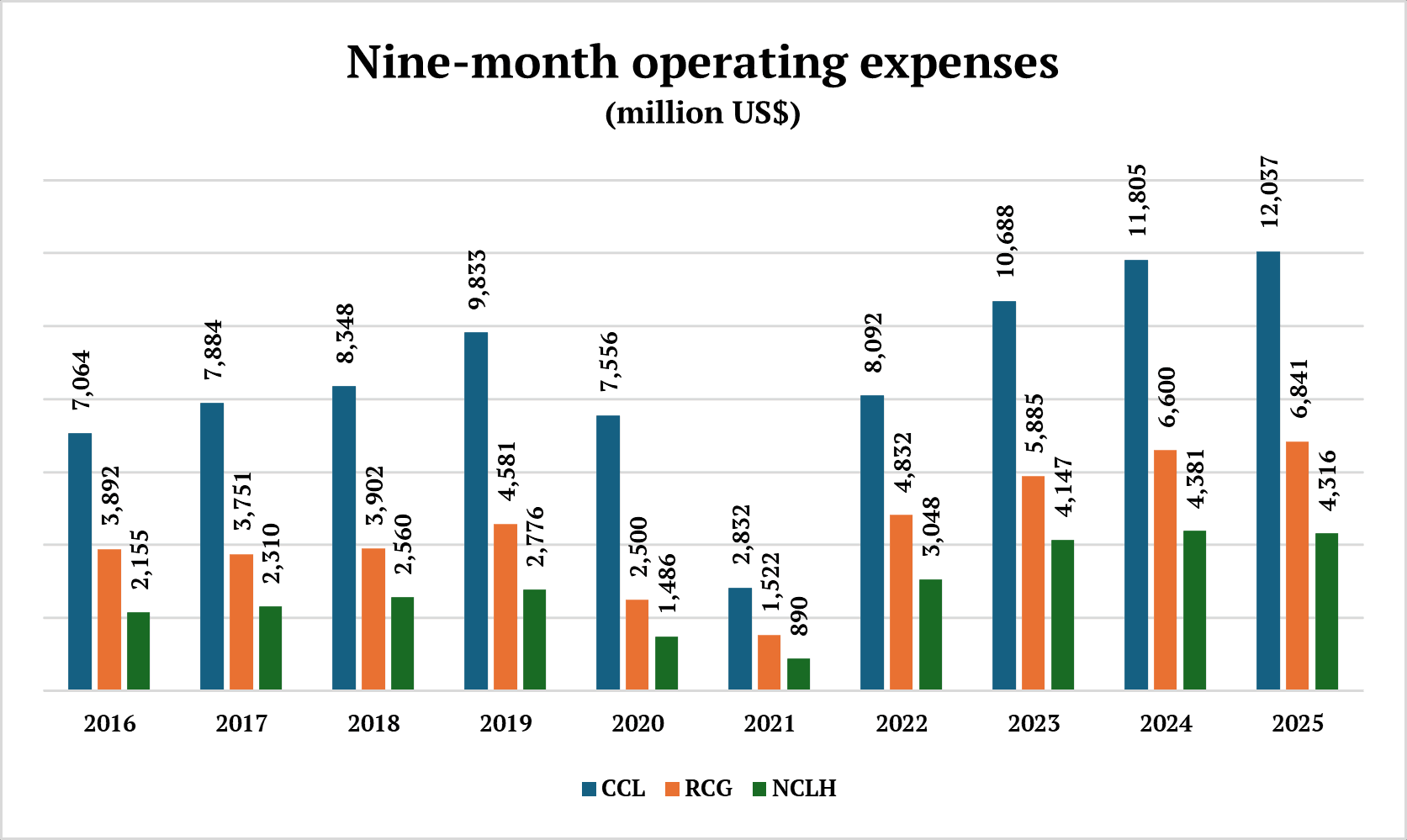

The major groups’ earnings performances continued to improve, driven by strong demand and helped partially by effective cost-efficiency drives.

The increases in operating expenses were slight in the nine-month period, with NCLH actually managing to reduce costs marginally, which might be attributed to a lower passenger number.

Source: CCL, RCG, NCLH

Source: CCL, RCG, NCLH

While the general slowdown may be disquieting, we must remember that the recovery in the immediate post-pandemic years was unusually vigorous. This is now moderated to a more natural and organic pace. What is important is to witness the continuing growth, albeit less explosive.

Part of the reason for the slowdown could be that growth and expansion were still being held back by the eye-watering debt accrued during the Covid-19 pandemic. This was addressed gradually and arduously.

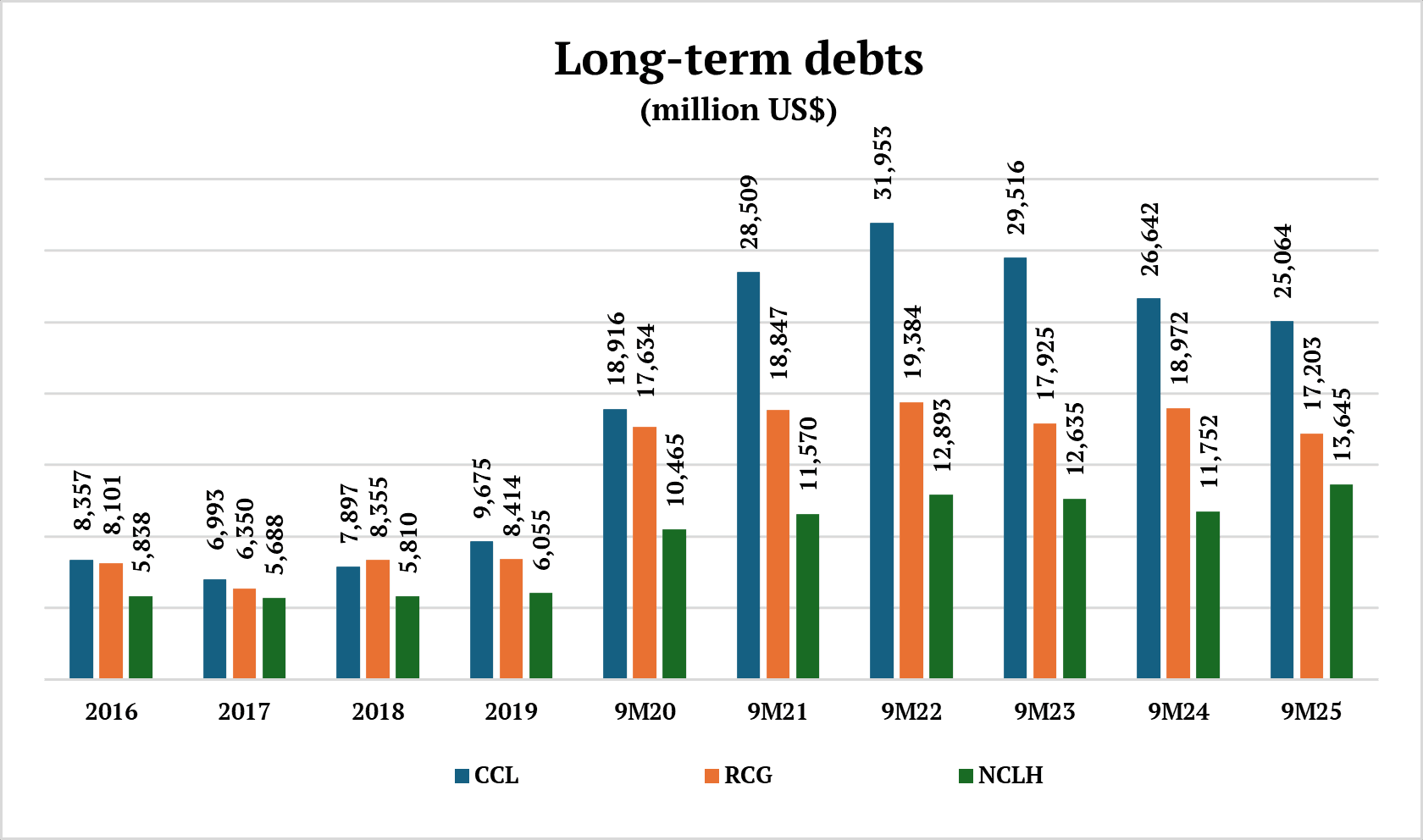

CCL’s long-term debt fell by 6% in the 12 months leading up to the end of August 2025. Some may say this was not fast enough in the high-octane cruise business of today. With its ambitious newbuilding programme that runs to 2033, CCL’s debt level will remain high for the foreseeable future, consistent with our previous forecast. But the group was confident about its debt-management strategy and the robustness of its balance sheet.

“With our current refinancing strategy nearly complete, we’ve continued taking decisive actions to strengthen our balance sheet by simplifying our capital structure, reducing interest expense, and managing our future debt maturities,” said David Bernstein, the group’s chief financial officer.

By the end of August, CCL has opportunistically refinanced over $11 billion of debt and prepaid another $1 billion. “Our focus is now on driving our net debt to adjusted EBITDA ratio to under 3x as we continue boosting our financial strength,” he continued.

RCG’s long-term debt fell by 9.3% in the 12 months leading up to September 2025 – a better performance.

In the same period, unfortunately, NCLH saw its long-term debt rising by as much as 16.1%. This is an unwelcome development, especially in the light of its continuing commitment to a huge newbuilding programme, which now includes four costly 226,000-gross-ton vessels.

But the overall picture of the sector, judging by the trio’s latest financial performances, is overwhelmingly positive, and a far cry from the existential struggle of just four years ago.